The value of a mortgage offset account

Most lenders offer mortgage packages which include a mortgage offset account. Although the benefits of a mortgage offset account may be attractive for some clients, they may involve higher fees, requiring some cost-benefit analysis.

This article aims to help you understand the situations where a mortgage offset account may be advantageous.

What is a mortgage offset account?

It’s really very simple. A mortgage offset account is usually a transaction or everyday banking account that is linked to a mortgage debt account. A client may contribute funds to the mortgage offset account at any time, but they must also meet their repayment obligations on their mortgage debt account.

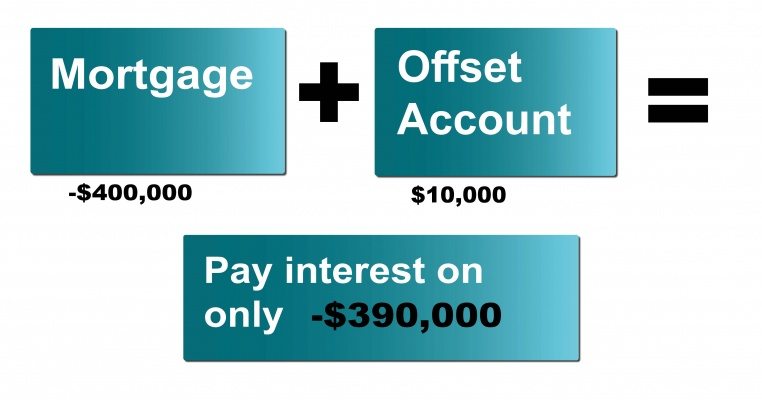

The balance of a mortgage debt account is used to calculate how much interest is payable, usually on a monthly basis. If there are funds in a linked mortgage offset account which offers a 100% offset, the balance of the mortgage offset account reduces the mortgage debt account balance that is used to calculate the interest payable.

Example – Matt & Jessica receive a lump sum:

Matt & Jessica are 33 and 34 respectively and have a mortgage of $400,000 on their home. Their mortgage arrangements are as follows:

Loan amount: $400,000

Interest rate: 4.0%

Loan term: 30 years

Repayment type: Principal and interest

Monthly repayment: $1,887.03

They have received a windfall of $50,000 and wish to use the funds to help pay down their mortgage as soon as possible.

Their options include:

- using the $50,000 to immediately reduce their loan debt

- depositing the amount into a separate bank account which pays interest of 2.0%, with the goal of using the balance later to reduce the mortgage debt

- depositing the amount into a linked mortgage offset account (the account incurs an extra $400 per year in fees) with the goal of using the balance later to reduce the mortgage debt.

Option 1 – reduce loan principal

With option 1, Matt & Jessica’s outstanding debt (that is, their ‘loan principal’) will be reduced to $350,000 by the payment of $50,000. Interest (at 4.0% per year) will be calculated on $350,000 rather than $400,000, so there is an immediate interest saving of $164 in the first month (assuming a 30 day month).

If Matt & Jessica maintain the same level of repayments per month ($1,887.03) their mortgage term will be reduced by six years and three months, and their total repayments will be reduced by $92,717 (equivalent to $24,565 in today’s dollars assuming a CPI rate of 2.5%).

However, it may be difficult for Matt & Jessica to redraw the funds if they wished to access the funds due to unforeseen circumstances. Some mortgage debt accounts allow extra repayments to be redrawn, but this is not always the case. Redrawing additional funds may require an application to the lender, with costs, and it may take some time before the necessary funds are available.

Option 2 – bank account deposit

Depending on the type of bank account used, option 2 may involve access to the funds at call or at short notice, and potentially at no costs. This may be comforting for Matt & Jessica, especially if their excess cash flow is limited after funding their existing lifestyle and mortgage repayments.

But this increased accessibility to the funds comes at a cost to Matt & Jessica when compared with option 1. The interest rate assumed to apply to the bank account (2%)is considerably lower than the mortgage debt account interest rate (4.0%. Furthermore, the interest earned on the bank account is taxable at Matt & Jessica’s marginal tax rates (37%), assuming the account is in joint names.

Option 2 reduces Matt & Jessica’s loan term by three years and one month, assuming they maintain the same level of repayments per month ($1,887.03). Their total repayments would be reduced by $23,392.

Option 3 – using a mortgage offset account

Option 3 involves depositing $50,000 into a mortgage offset account, rather than a separate bank account. The facility costs $400 per year.

The benefit is the reduced interest on the debt account the mortgage offset account is linked to. By offsetting the interest payable on the debt account, effectively the mortgage offset account generates an after-tax return of 4% for Matt & Jessica. To achieve the same result, the separate bank account in option 2 would have to pay interest at 6.56% (assuming Matt & Jessica’s marginal tax rate is 37%.

Option 3 reduces Matt & Jessica’s loan term by five years and three months, assuming they maintain the same level of repayments per month ($1,887.03). Their total repayments would be reduced by $71,654 (equivalent to $12,825 in today’s dollars assuming a CPI rate of 2.5%).

A key advantage of a mortgage offset account in this situation is Matt & Jessica’s ability to redraw the funds at short notice. With some offset accounts, access to the funds is immediate. So, if Matt & Jessica encounter unforeseen expenses, such as major house repairs, they may be able to draw on the required funds from their mortgage offset account. The potential to immediately draw on funds can be very comforting.

In summary:

Option 1 would result in Matt & Jessica paying off their home loan in 23 years and nine months.

Option 2 would result in Matt & Jessica paying off their home loan in 26 years and eleven months.

Option 3 would result in Matt & Jessica paying off their home loan in 24 years and nine months.

The motivating impact of a mortgage offset account

Some clients may be reluctant to make additional payments towards their mortgage debt where they feel they are losing access to those funds.

The generally immediate access to funds placed in a mortgage offset account can provide a strong incentive to further increase the flow of funds into a mortgage reduction arrangement. Motivated clients may be inclined to maximise the use of their mortgage offset account by directing all cash flow, including their salary, through their mortgage offset account, and making expense payments from it. This strategy will further reduce the amount of interest they pay over the term of their home loan.

Another example – Matt & Jessica use excess cash flow through the offset account

Matt & Jessica decide to run all their excess cash flow through their mortgage offset account. They both earn $90,000 per year before tax and require $6,500 per month for their day to day living expenses.

Their excess cash flow (approximately $2,800 per month, increasing over time) accrues in the mortgage offset account, reducing the interest calculated on their home loan. As a result, Matt & Jessica are able to pay off their home loan 23 years sooner than under their original loan term of 30 years. Their total repayments would be reduced by $226,851 (equivalent to $61,548 in today’s dollars assuming a CPI rate of 2.5%).

Mortgage offset accounts can also be beneficial for investment property loan arrangements, where the interest expenses are tax deductible.

Placing additional funds, such as windfall lump sum, into a mortgage offset account will reduce the interest expense broadly to the same extent as paying down the loan principal.

The advantage of using a mortgage offset account is that if the funds in the mortgage offset account are withdrawn later, for an overseas vacation for example, the increased interest payable as a result of the withdrawal may be tax deductible if the income producing purpose of obtaining the loan still remains.

In contrast, if the windfall was used to reduce the loan principal, and subsequently redrawn to fund the overseas vacation, the interest on the loan would be only partially tax deductible, as the redrawn funds would not be for income producing purposes.

Conclusions

Mortgage offset accounts are a useful strategy for both home loan borrowers and investment loan borrowers. Although they may involve additional fees, the long-term benefits will often outweigh the additional cost.

Leave a Reply

Want to join the discussion?Feel free to contribute!